The calling card of all cryptocurrencies is instability. One could make millions or lose everything in the blink a billionaire’s tweet. Volatility can be great if you’re someone who understands how to use this as an advantage but most people don’t. Volatility is one of the main reasons cryptocurrency has not gained wider adoption. No one wants to be the guy who paid 10,000 bitcoins for 2 pizzas.

Enter Stablecoins

Volatility was also a problem for crypto traders and the introduction of a crypto version of a sable asset created a much needed way to hold cryptocurrency in some stable medium.

Stablecoins are used as a way to preserve and store fiat value in crypto format. Instead of risking any gains being lost, traders could just swap the cryptocurrency they made into a stablecoin without having to physically cash out of the market. Stablecoins also made it possible to buy and sell goods and services in crypto without having to worry about minute-to-minute price swings.

How stablecoins get their value

A stablecoin relies on a more stable asset as the basis (collateral) for its value, similar to how the USD dollar was pegged to the gold. If a stablecoin holder wants to cash out their stablecoins, the amount they is the same value, just in the form of the stable asset. There’s a 1:1 relationship between the stablecoin and the asset that collateralizes it.

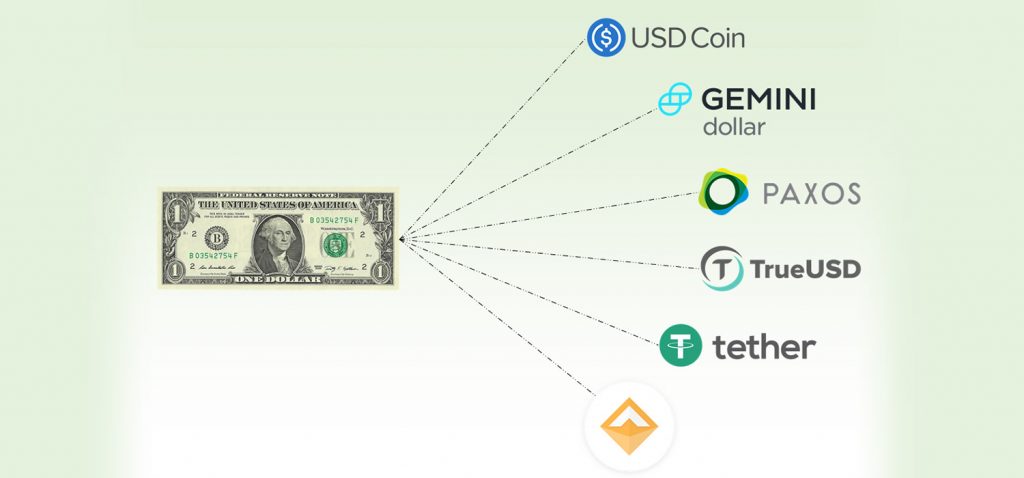

While there are some stablecoins that are collateralized (backed) by an asset like USD, this is not the case for all. There are 3 main types of stablecoins, each using a different method of collateral.

| TYPE | ABOUT | PROS | CONS | EXAMPLES |

| Fiat Backed | Pegged to and backed by a specific, centrally managed asset like USD. | – Safe against crypto volatility – Changes in price are minimal | – Requires centralized banking structure – Requires auditing to ensure sufficient reserves | USDC Tether BUSD |

| Crypto Backed | Backed by other crypto assets, and must be over-collateralized to hedge against instability | – Transparent, fully decentralized. – Quick to turn into other crypto assets – No external custody, all done on blockchain | – Crypto is volatile – Requires close watch – No centralized management structure | DAI |

| Algorithmic | Not backed by any assets. An algorithm manages the price and maintains the value | – No collateral needed – Controlled by a public algorithm | – Faith in the algorithm – Balance of coins changes based on total supply | UST USDD |

The role of decentralization

The notion of decentralization has been one of the biggest draws and drawbacks of cryptocurrencies. While the proponents of decentralization evangelize the pros, you can see from the table above that’s it’s just as easy to come up with the opposing cons. Trust of any centralized entity goes against the ethos of cryptocurrencies, and algorithmic stablecoins (in theory) are one of the few ways of achieving both decentralization and price stability.

But how a stablecoin handles collateralization is where things start to differ. In the case of an algorithmic stablecoin, how do you convince people that something is a stable investment if the whole foundation of it’s value is based on something that also has no inherent value? And that this value, however it gets created, will all be managed by an algorithm?

Enter TerraLuna

Terraform Labs was started in 2018 by a South Korean duo. Do Kwon, the younger half, was a Stanford computer science grad who briefly worked at Microsoft but left only after a short stint to seek greater challenges. He first started a mesh networking company which led him to blockchain and the story to come.

Daniel Shin was a Wharton grad who had already established himself as the founder of one of South Korea’s first e-commerce platforms called Ticket Monster (TMON). When he met Do Kwon he’d already sold TMON to Groupon for $260 million and was looking for the next thing. His commercial instincts and knowledge about payment processors, e-commerce and connections were exactly what Do Kwon needed and proved to be valuable in their rise.

In the beginning, TerraLuna was one of the most promising and ambitious crypto ecosystems. Their mission was to “the most useful dollar possible”. But without the backing of a real and accepted asset like USD or gold, the only way to get people to use it would be to make it something that people would find hyper-useful in their daily lives.

The Terra Blockchain would need to do a few things really well in order to gain the mass adoption needed to scale.

- Facilitate payments – people need to be able purchase goods and services. Merchants need to be able to accept payments.

- Pay interest – people should be able to generate interest from any money they store.

- Invest and borrow – people need ways to invest in different asset classes and use their existing wealth to increase it

They knew that the fastest path to growth would be by focusing on solving real world problems and create value for the masses. This was also the only way to gain mass adoption create multiple customer demand streams.

The success formula

In order to succeed, Terra required two things of their stablecoin:

- Price stability

- Mass adoption

The Terra Blockchain proposed maintaining stability via a two-coin approach using these two coins:

| UST | LUNA |

| The stablecoin which maintains its peg to the US dollar value through an arbitrage mechanism with LUNA | The native governance token, transacted upon to accrue rewards (profit) |

Arbitrage between the two coins would be the mechanism to maintain the price stability of UST.

Stability

Terra claims that the elasticity of LUNA’s supply (and the profit you can make through arbitrage) means that the stablecoins will never fall out of balance.

It achieves price-stability via an elastic money supply, enabled by stable mining incentives. It also uses seigniorage (profit from minting money) created by its minting operations as transaction stimulus, thereby facilitating adoption.

Terra Money White Paper

What they’re saying is that people will always want to make money AS LONG AS they believe there’s money to be made. So in order for UST to keep it’s value at $1 USD, an arbitrage opportunity must exists and it needs to be used. If for whatever reason people lose enthusiasm and stop buying Luna, UST would lose it’s peg, more people would see this and sell off their Luna and the whole system would basically collapse.

Mass Adoption: dApps

The other half of the success equation was getting mass adoption, also outlined clearly in the Terra white paper:

…price-stability is not sufficient for the wide adoption of a currency. Currencies inherently have strong network effects: a customer is unlikely to switch over to a new currency unless a critical mass of merchants are

Terra Money White Paper

ready to accept it, but at the same time, merchants have no reason to invest resources and educate staff to accept a new currency unless there is significant customer demand for it.

Terra knew that it needed strong ‘network effects’ to achieve growth at scale. Building dApps on top of the Terra Blockchain was the way they did it.

dApps – are “decentralized applications” built to work on top of a blockchain network. dApps have become a way to for new audiences to experience and use blockchain technologies via an interface that looks just like other common web apps apps.

Chai

CHAI was Terra’s consumer payments platform that offered a seamless payment experience similar to a PayPal or an ApplePay. Users simply sign up and connect their bank or credit card. Behind the scenes, though, Chai utilized stablecoins minted on the Terra blockchain to process payments, a drastic departure from any other payments app on the market.

By making it super simple for both consumers and merchants to onboard and use, Chai processed $2 billion in transactions and had over 2.5 million users and 2000+ merchants in 2020. Even Nike in South Korea used Chai.

Playing a critical role in accelerating the adoption of Terra stablecoins in real life, payment processing with CHAI was so easy that its users had no idea it had anything to do with blockchain.

Mirror

U.S. equities are an attractive asset class globally, but access to anyone outside the U.S. is limited. Mirror was a ‘synthetic assets’ protocol that enabled investors outside the U.S. to easily participate in U.S. equities markets by creating tokens that could be traded as mirrors of the financial product without actually buying it directly.

Synthetic stocks were listed in the Mirror app using an ‘m’ in front of the company name. To mint (buy) mAssets, users would use UST as collateral. While somewhat short-lived, this was another great example of use of the Terra Blockchain and another way to get people using UST.

If you’re also having a have a hard time wrapping your head around this concept makes sense you’re not alone, the SEC seemed to agree and has subpoenaed Terra in an investigation into potential violation of federal securities laws by allowing synthetic stocks to be minted and sold on its platform.

Anchor

But if there was one thing that supercharged Terra’s growth it would be Anchor. Anchor was essentially a ‘savings’ protocol, explained best by Do here:

“Anchor’s attractive yields on TerraUSD is going to lead millions of households to move their savings onto Anchor’s smart contracts, and will bring DeFi from the fringe to the mainstream.”

Attractive yields they certainly were, to the tune of 20% APY. Just for context, Bernie Madoff was returning a paltry 10%. Anyone could open what was essentially positioned as a high-interest savings and lending account by simply signing up via the website and transferring funds from their bank to Anchor.

Word spread fast and as expected, millions created accounts and many moved their life savings into Anchor, the ‘gold standard for passive income on the blockchain’. But how exactly did Terra plan to maintain these amazing returns? and pay them out if people decided to take their money out?

And if a decentralized system was working as expected, how would it even offer such a high interest rate? And wouldn’t it have been impossible to maintain such a rate anyways?

As perfect as the plan sounded, the fact was that Terra was subsidizing the interest from the start and couldn’t afford to turn it off without risk of triggering a mass exodus of people pulling their money out of Anchor. So rather than let the market do it’s job, Do Kwon continued to subsidized the interest, at one point payout out as much as $7 million a day in interest.

While the going was good, people kept putting money in and the needle kept moving higher. At its peak, UST had over $18 billion USD in circulating supply and Anchor, over $15 billion USD.

The #Lunatics

Terra had their share of skeptics and detractors, many of whom were not afraid to call Terra out as a ponzi.

Thanks to Do Kwon’s baller Twitter personality he was able to use these opportunities in the public forum to shut down the haters and stoke the fire of the rapidly growing community of believers at the same time. It’s somewhat ironic looking back that they called themselves #Lunatics.

Here are some of Do Kwon’s best tweets.

In response to @AlgodTrading’s short call in early March:

And again a few days later making bets:

He also referred to his critics here as ‘poor’?

Shading the competition, $DAI, another algorithmic stablecoin:

And if you thought it was a scam, would you really do this?

And if you still doubted, even after seeing baby Luna, would an experienced investor like Mike Novogratz actually be doing this?

In hindsight it’s probably easy to say that none of these examples create a sound foundation for judgement but at at the time, over time they probably did a lot to reinforce the message and create more #Lunatics – a community that was essential to helping get more people onboard.

The LFG

While Do Kwon used Twitter as a tool to flex and rally both the lovers and the haters also knew that the risk of a black swan event was real and needed to make sure he had a way to maintain the peg in a pinch.

In February he announced the creation of the Luna Foundation Guard (LFG) which was a non-profit with a noble sounding yet vague-ish mission to

Create and provide greater economic sovereignty, security, and sustainability of open-source software and applications that help build and promote a truly decentralized economy.

via: LFG.org

But LFG was essentially created and run by Do Kwon so it was more for optics purposes to show how committed he was to keeping TerraLuna going. He announced on Twitter that in the case there ever became a situation where UST started to lose its peg, LFG would have a stockpile of Bitcoin (BTC) as a reserve currency to buy UST and restore the peg.

At one point LFG had so much Bitcoin they became the second largest corporate holder after Tesla.

What could go wrong?

It’s unclear to me why one would choose a volatile asset like BTC for collateral purposes. In general, cryptocurrencies typically move together (they move up and down together) so if the LFG Bitcoins would ever need to be deployed to save UST, the value of those bitcoins would likely also be losing value at the same time making it harder to bring the peg back.

For a while the algorithm seemed to be working perfectly and everything was fine, until it wasn’t. There are several theories as to what happened to UST back in early May. Some say it was a deliberate and coordinated attack by but it’s also entirely possibly that it was an organic and inevitable unravelling.

Gemini, the cryptocurrency exchange started by the Winklevii, were swift to put a cap on rumours they had anything to do with it:

Regardless of how it all started, LFG intentionally hoarded Bitcoin for this specific purpose. The often touted benefit of cryptocurrencies is the transparency of blockchains. You may not know who is behind the transactions but you can follow them live. For UST this probably worked against them to exacerbate the problem once outflows started.

The beginning of the end

On May 7th there was a trade of 84.5 million UST for USD Coin, another stablecoin. There were also massive withdrawals from Anchor.

Once news of these big trades caught wind, the price of UST dropped slightly but LFG was able to deploy their Bitcoin to help bring it back up. But being one of the largest holders of Bitcoin, as they started to sell more to restore the peg the price of Bitcoin started to fall. Coincidence or not, there was also a big short out on Bitcoin at the time which added more fuel to the theory this was a coordinated attack.

Within days, the big panic is at full speed and the dreaded “death spiral” begins. Arbitrageurs redeemed UST for Luna which they then sold, leading to a significant decrease in its price, which necessitated more Luna being minted for each UST burned, creating a hyper-inflationary loop in Luna’s supply.

Within a week of UST starting to lose it’s peg it was all over.

Just keep swimming

There have been some deep dives into the transactions and timings of those transactions when the collapse started. No one, however, has been able to provide enough evidence about who it actually way.

Not even a month had passed before Do announced the launch of the revival, Terra 2.0

While crypto has certainly attracted it’s share of greedy scammers, the people who lost the most were regular people looking for a way to get ahead. And most, if any, will never get their money back.

To me it’s a bit surprising to see how quickly people move on but i think it’s also a reflection of how the crypto sector operates. And while the TerraLuna crash is still being processed, it appears as though the impact has been felt by other big players and I suspect we’ll learn more about if and how they’ve been affected in the coming months. And of course none of this is to say that the other stablecoins as stable as they claim, Tether has had it’s share of challenges and continues to exhibit speculative traits despite continuing to position itself as a stable investment.

Personally I’m excited to see where these how we can use these experiences, although negative in the short-term, as an input to our learning around the real life application potential for cryptos, dApps and blockchain ecosystems. But in the meantime, for anyone expecting to get a 20% return without taking a huge risk, the story of TerraLuna should be one that’ll make you think twice.

Leave a comment